Dr. John F. Clayburg

Creating Self-Adaptive Trading Systems using

Parallel User Functions

TradeStationWorld

Session

Self Adaptive System Slide Presentation

Use this link to download the free Self Adaptive System

presented at TradeStationWorld

Self-Adaptive Systems EasyLanguage

Code and Free Indicator Trial

Contact

Information

.......

"Self Adaptive

Systems"

A "Self-Adaptive

System" is quite simply one that has the internal ability to dynamically

alter its analytical equations in real time to more closely adapt the system to

ever changing market conditions. The systems accomplish this task by the

diligent application of parallel functions.

What makes Parallel User Function driven systems unique?

Recall the old college days, just after that chemistry exam when you realized

you should have spent more time reviewing the section on oxidation and reduction

and less time on electron shell configuration? Or after the English exam when

you found the test emphasis on sentence construction rather than proper pronoun

usage, which you had spent all night studying?

How about that last trade, when just waiting a few more minutes for your entry

or exit would have turned the result into a profitable experience rather than

another one of those annoying losses?

Obviously, its not possible to turn the clock back and alter previous

decisions. However, we have all, hopefully, over the years, learned from our

previous experiences and have become better traders as the result of this

learning process.

Parallel Function Technology operates in much the same fashion as our own

learning process. While there is no computer in existence, or even on the

horizon, which can come close to the analytical capability of the human mind, we

can, with our Parallel Function Technology, enable our trading systems to learn

from their past experiences and become more effective as a result.

The ultimate objective of all trading is to buy the low and sell the high. As

you know this is much easier said that done. In fact it is, in all likelihood,

altogether impossible. It is possible however to buy and sell in areas where

price action determines that the trade has a higher probability of being

profitable rather than losing.

In this attempt, our Parallel Function based systems are always trying to

identify optimum buy and sell areas. If the identification of this buy and sell

area can be improved upon, the system recognizes this fact and will

self-adapt to take this new understanding into account the next time a

similar market situation arises.

For example, lets consider a trade placed by the Universal System. A

set of specific mathematical equation is used to calculate all trading

signals.

Obviously, all the signals from this system are not perfect. In many instances,

moving the entry point forward or back a few bars would improve the quality of

the signal issued by this trading tool.

Using historical data, we can easily determine the top or the bottom of the

price move where the placement of our buy or sell signal would have been

optimally placed.

The system component of our Parallel Function programming examines the

relationship of all the orders placed over a given period of time and compares

the placement of the signals to what would have been the perfect placement of

each order. The computer program then makes alterations to the base system

equation in an attempt to more accurately place the proper buy and sell signals

as they are issued by the system when similar chart patterns present themselves

in the future.

One might ask, at this point, with the self-adaptive nature of this system

discussed above, why all the signals arent always perfect after the

examination of an adequate amount of past data. The best answer to this question

requires a more detailed examination of the forces that are responsible for the

creation a price chart.

Price charts are ultimately the expression of random human behavior in the

market place. Much of this random activity is largely the result of analytical

inputs, such as supply and demand, earnings and other hard numbers which are

objective in nature and can be analyzed mathematically. The balance of the

origin of market behavior is the result of human emotion, intuition and other

non-analytical data and therefore much less repetitive and much more difficult

to analyze from an objective approach.

It is relatively simple to analyze, from a mathematical perspective, activity

which arises from the repetitive activity generated by hard data.

It is quite difficult, if not impossible, to objectively analyze and therefore

predict the subjective result of emotion and intuition.

Ultimately, therefore, it is mathematically possible to only predict a portion

of the activity which goes into the creation of a price chart. In a sense, you

are always shooting at a moving target from a mathematical standpoint, thus

markedly decreasing the accuracy of perfect market prediction.

However, with all of the above qualifications, the Parallel Function Technology

which drives all of the Systems offered on this site has been shown by our

research to be much more responsive to the ever changing conditions of todays

active markets than the standard indicator packages which use fixed mathematical

processes to calculate their respective buy and sell signals.

Background

It is a common observation of

experienced traders that markets are a constantly evolving, ever changing

dynamic. A myriad of fundamental factors as well as random human behavior

cause markets to constantly change their basic characteristics. After all, a

price chart is nothing more than the graphical description of the

multiple factors that effect prices.

The creation of automated

trading systems is often compromised by these changing market conditions.

The challenge then becomes one of designing systems that are, in one

fashion or another, able to change their characteristics automatically

in response to frequent market changes.

Presented here is a relatively

new concept in automated system design that enables a system to dynamically

alter its internal equations to more accurately keep page with the ever

changing landscape of today's active, volatile markets.

Introduction

This presentation is designed to detail an additional tool which

can be used to make trading systems more self adaptive and therefore more

responsive to current market conditions.

If a system uses back data in any manner it can be regarded as

being self adaptive to one degree or another. Moving averages, standard

deviations, breakouts, neural networks, etc. all rely on some historical

price movement to generate buy and sell signals.

This programming technique takes the self adaptive concept one

step farther by using the system itself to adjust its own trading parameters

for each trade.

I wish to emphasize at the beginning that this is a programming

technique which must be applied in a different manner to each and every

system on which it is used. It is not a canned function or add on program

which can be applied to any system.

Also, since the programming involved in the application of this

technique can be quite involved and extensive, it should be emphasized

that this is not a fix - all for mediocre or poor systems. In fact, it

will probably worsen the results of a poor system since the variables will

constantly be reset to extreme values, making the equity swings of the

system even more pronounced.

Systems which respond best to this technique are those which

are considered robust in nature and remain profitable over a progressive

set of input variables. Such a system should show a bell curve pattern

when the results of an optimization over the critical inputs is performed.

Systems which respond well to frequent optimization will find this technique

useful in improving performance and smoothing out equity curves.

Back Test Regular Optimization

Traders and system developers regularly check variations of their

system against recent back data in an attempt to discover if an underlying

change in the market has effected the performance of their system. Done

properly, this effort can be rewarded with improved system performance

real - time. Improperly done, which is more often the case, frequent re

- optimization leads to a system which is overly curve fitted and more

prone to losses.

The difficulty is knowing how often to optimize, over what system

parameters and how much data should be used for each test. To come up with

the correct testing parameters is a time consuming operation since there

are so many variables to consider. Also, if the testing is to be accurate,

a fairly large volume of past data should be considered.

Through the use of parallel functions, one can set up a group

of indicators which will graphically depict to the user when a significant

change has occurred in the manner in which the system is responding to

changes in market personality. Additionally, if warranted by indicator

observation, the system can be altered to automatically change variable

values when indicated by changes in the market.

In this manner one is able to observe what the results of the

system would have been had re-optimization occurred at regular, defined

intervals over specified input values.

Developmental History

When I began designing systems for currency trading in TradeStation

several years ago I was quick to notice that the optimal variables which

controlled the system equations would vary greatly from one contract month

to another. My initial methodology involved an early range breakout system

for trading the currency markets whereby the system would place breakout

buy or sell stops slightly outside the early market range. Since the definition

of the early range was critical to system performance, variables were used

in the system to set the range by time of day, width of the early range,

and the proximity of the current price to extreme range when the early

range was defined.

It was soon obvious that the best settings for the variables

used to define the critical early range varied significantly from contract

to contract. Even averaging the variables over several contracts produced

only mediocre results. Obviously there was a characteristic somewhere in

the activity of the market that was fluctuating regularly which resulted

in the radical activity of the system. Also obviously, if the system was

to be profitable in the future, I was critical to get a handle on the root

of these fluctuations. One could always optimize the variables for each

contract and make the system look like the best thing around but we all

know by now that curve fitting is a quick way to overconfidence and a losing

system.

For months I analyzed every market parameter I could define - gaps,

average daily range, daily open to close, ratios of high to low to open

to close, tendency of a quiet day to follow a wild day, changes of market

activity around big report days, and so on. Although measuring these parameters

and using them to adjust the system variables was of some benefit to system

performance, I was still unable to achieve the consistency across all data

that I desired.

Then one day it dawned on me - the best way to evaluate the market

with respect to a particular system is the system itself! By running the

system against a defined subset of past market data using a defined set

of variables one could constantly monitor the performance of the system

across all variable settings. Properly programmed, the system could constantly

adjust critical variables to reflect optimum performance against recent

market data.

This technique operates in much the same fashion in which the pure

market technician assesses the market. The pure technician ignores all

fundamentals, confident that eventually all forces impacting on the market

will be reflected in price. In much the same way, a parallel user function

ignores all the myriad of technical forces in the market as they impact

the system and concentrates only on the net effect of these changes in

market characteristic on the system itself. Rather than trying to determine

which phase of market activity is impacting the results of the system,

we use the system itself to monitor changes in the market personality and

make system adjustments accordingly.

To accomplish this formidable task I created what I have chosen to

call the Parallel User Function Approach to System Design.

What is a "Parallel

Function"? In the

TradeStation platform, it is possible to program multiple subroutines, referred

to as user functions, which process data "outside" the main system

program, making the data generated in the function available to any program

which calls the function. A

"Parallel Function" is simply a TradeStation user function programmed

as a system. Although the actual programming is significantly more complicated

than that used to create an actual strategy, these functions allow the base

system to actually self test itself against current market conditions and then

utilize the prime system settings. In

this fashion the base trading strategy is able to change its critical parameters

and equations "on the fly" and therefore be much more responsive to

the regular changes in market personality that plague most non adaptive systems.

How Does It Work? Self

adaptive trading systems gain their advantage by continually testing themselves

against nearby market data using parallel function technology. The parallel

function is effectively running multiple systems in the background. By passing

multiple levels of system inputs to the parallel function the base strategy is

able to monitor the current behavior of the system against a wide array of input

patterns. A simple sort routine then enables the base system to utilize

the most effective input combinations for current trading. In

this fashion, no matter what outside forces are causing regular changes in

market personality, a self adaptive trading strategy utilizing parallel function

technology is able to effectively alter its signal generation process to create

a trading atmosphere more in line with the current market. Building

a Self Adaptive System The

first step is obviously creating the parallel function. Care must be taken to

assure that the function creates exactly the same returns as the base system -

otherwise the function is useless as a trading aid. Programming these functions

is more than a little complicated since many of the reserved words, such as buy,

sell, buy to cover, sell short, etc. may not be used when programming a

function. Next, within the

parallel function or in another linked function, you must set up a routine to

test all the system input combinations passed to the function from the base

program. If you intend to use for - next loops to test and sort these inputs

care must be taken to create the parallel function as a simple function as

opposed to a series function which refers to a previous value of itself

somewhere in the routine. Series functions are not able to be used in loops in

easy language. Then, usually

in the parallel function, it is necessary to set up a sort routine to isolate

the best performing set of system variables from the group passed to the

function from the base system. Finally,

one must create a routine within the base system to retrieve the sorted system

variables from the parallel function and properly replace these critical values

for the next series of trades. Retest

Options Critical to the

profitable performance of a self adaptive system are the parameters which govern

the periodic retesting of the system which immediately resets the system

variables. The timing of these retests and the range over which the system is

allowed to test itself will be critical to the eventual profitability of the

resulting strategy. In the

example coded provided on this site, you will notice a "reset" input

on the strategy for each parameter. In this example, I have allowed the system

to reset each of the three system inputs independently. It is obviously also

possible to reset all variables simultaneously. The

frequency of retesting and the range of inputs over which to run the test is

strictly dependent on the nature of the underlying system. While the example

system seems to respond to very frequent retesting of all parameters ( 2 - 5

days currently ) other longer term systems will probably respond more

effectively to a longer retest interval. I

would suggest that a manual walk forward system optimization exercise would be

the most efficient manner to determine the effective retest frequency and input

ranges for any system to which this routine is to be applied. Using

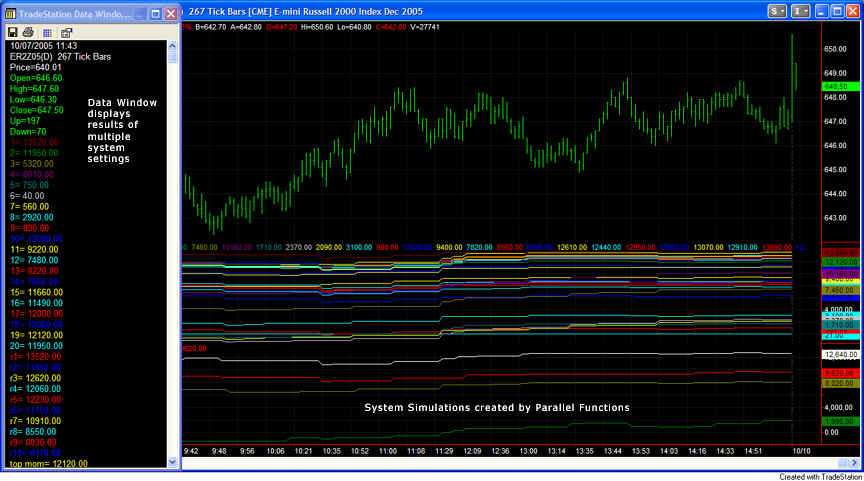

the Parallel Function as an Indicator A

parallel function may also be utilized as an indicator to plot the result of

multiple system settings. Those not wishing to take this technology to the fully

automated level may, in this manner, visually observe multiple settings of the

system and use this information to manually make appropriate changes to the

system being used for trading.

In

the chart above note the multiple plots below the price graph which display the

real time equity curve of 30 separate system settings. The data window to the

left of the chart reveals the current profitability of each graphed system

setting. Although this use

of parallel functions visually displays multiple system settings, the user must

realize that these plots are the result of fixed input settings and do not offer

the analysis of the range of system inputs that can be dynamically created by

the automated parallel function system. Limitations Parallel

functions are not a cure all for all systems. One must be certain that an

effective trading strategy lies behind the logic of the main system. A robust

system is a must before this technology should be applied. In

fact, this theory will probably only make an ineffective system worse. Additionally,

this is not a technology that can be applied as a "canned" function to

any system. It must be specifically designed for each system to which it will be

applied. Conclusions While

parallel function technology is difficult to apply and will not be suited to all

system designs, the advantages of using the system itself to direct appropriate

changes in critical system parameters are readily apparent when the technology

is properly designed and applied. More

information is available from the slide presentation used to present this topic

at the TradeStationWorld conference in Las Vegas, Nevada, September 30 - October

2, 2005.

Click here for further information.

|