|

1

|

- Presented by Dr. John F. Clayburg

- www.clayburg.com

|

|

2

|

- Each speaker at the TradeStationWorld Conference acts independently,

and no speaking topic, session, seminar or content is affiliated with,

or approved, sponsored or endorsed by, TradeStation Technologies, Inc.

or any of its affiliates. Topics, sessions and seminars are solely for

educational purposes. The speaker roster and session/seminar content are

subject to change without notice.

No investment or trading advice regarding any security, group of

securities, market segment or market is intended or shall be given. Any

examples used in sessions, seminars or speaking topics are for

illustrative purposes only -- they should never be construed as

recommendations or endorsements of any kind. No particular trading strategy,

technique, method or approach discussed will guarantee profits,

increased profits or the minimization of losses. Past performance, whether actual or

indicated by simulated historical tests, is no guarantee of future

performance or success.

Testimonials may not be

representative of the experiences of other customers and are not

indicative of future performance or success.

- TradeStation

Technologies, Inc., the host of the conference, and TradeStation

Securities, Inc. (Member NASD, SIPC and NFA), the conference's premier

sponsor, are affiliated companies. "TradeStation," as used in

this presentation, refers to the trading analysis software products,

platforms and services that have been developed by TradeStation

Technologies.

|

|

3

|

- This presentation will explain

in detail several, specific, practical approaches to system design that

will assist traders by designing systems that can keep pace with current

market conditions.

|

|

4

|

- 1. Visual approach.

- 2. Semi automated approach using parallel function based indicators.

- 3. Totally automated approach.

|

|

5

|

- Before we proceed….

- Consider that when creating automated trading systems we are effectively

attempting to mathematically predict human behavior.

|

|

6

|

- Remember that technical analysis

is not a world of absolute certainty….

- But a world of probabilities and possibilities

|

|

7

|

- Background

- Automated trading systems use

certain values that define critical system calculations and therefore

control system performance.

- These values are fixed within

the system structure and do not change unless alterations are done

manually.

|

|

8

|

- Unfortunately, the best values

for these inputs can vary considerably as markets change and evolve over

time.

- Optimal results are not

produced by the system since the key values for the system remain fixed.

|

|

9

|

- For example, a system using a

simple moving average crossover may give the best profit picture in the

March contract of the e mini s&p using values of 9 and 18 for the

two moving average settings.

|

|

10

|

- However, when the same system

is applied to the June contract radically different settings may be

required to return the desired results.

- Unfortunately, the system does

not return the best results since it is still using the 9 and 18 values

for the system inputs.

|

|

11

|

- What changes in the markets are

responsible for the varying responses of trading systems?

- Volatility?

- Emotion?

- Greenspeak?

- Politics?

|

|

12

|

- Who cares.

- All fundamentals are eventually

factored into price anyway.

- The pure market technician only

analyzes price action to generate trading signals.

|

|

13

|

- In the same fashion, the parallel

function / self-adaptive approach to system design ignores the actual

market fundamentals that cause the system to respond differently during

different time frames.

|

|

14

|

- The results of these changes in

market personality will be reflected in the actual system results.

- Use the system itself as a diagnostic routine.

|

|

15

|

- Effectively, we are using a version of the system itself to tell us what

the best system settings are for the current market conditions.

|

|

16

|

- While the purpose of this presentation is to discuss the creation of

automated self adaptive systems, there are other, simpler methods to

keep a system in sync with the market.

|

|

17

|

- Several methods:

- Visually monitor multiple settings

- Re-optimize the system

- Automate the system to a greater degree

|

|

18

|

|

|

19

|

- 2. Re-optimize the system

- When trading results begin to deteriorate

- On a regular schedule.

- Danger of curve fitting the system to historical data.

|

|

20

|

- Another method used to keep a system trading profitably through changes

in market personality.

- Self – Adaptive Parallel Function Automation

|

|

21

|

- In the same manner that market

technicians focus only on price action to make their predictions, the

self – adaptive parallel function approach to system design focuses only

on the response of the system to varying market conditions.

|

|

22

|

- Self – adaptive systems change

their critical trading parameters

“ on the fly “ to assure the use of the most productive system settings

for the current market.

|

|

23

|

- This unique approach to

automated system design effectively uses the system itself as an tool to

decide which system settings are appropriate for the current market.

|

|

24

|

- What is a “Parallel

Function”?

- A Function programmed as a system.

- Allows the user to monitor system performance over a range of input

variables.

- Can be used visually when plotted as an indicator

- Can be used in actual system code to reset system variables as current

market conditions indicate

|

|

25

|

- Using a Parallel Function as an

Indicator

Indicators will graphically interpret when a significant change

has occurred in the manner in which the system is responding to changes

in market personality.- The user has the ability to create any number of simulated systems which

will plot as an indicator.

- It is possible to observe which system settings are the most profitable

at any point in the chart.

|

|

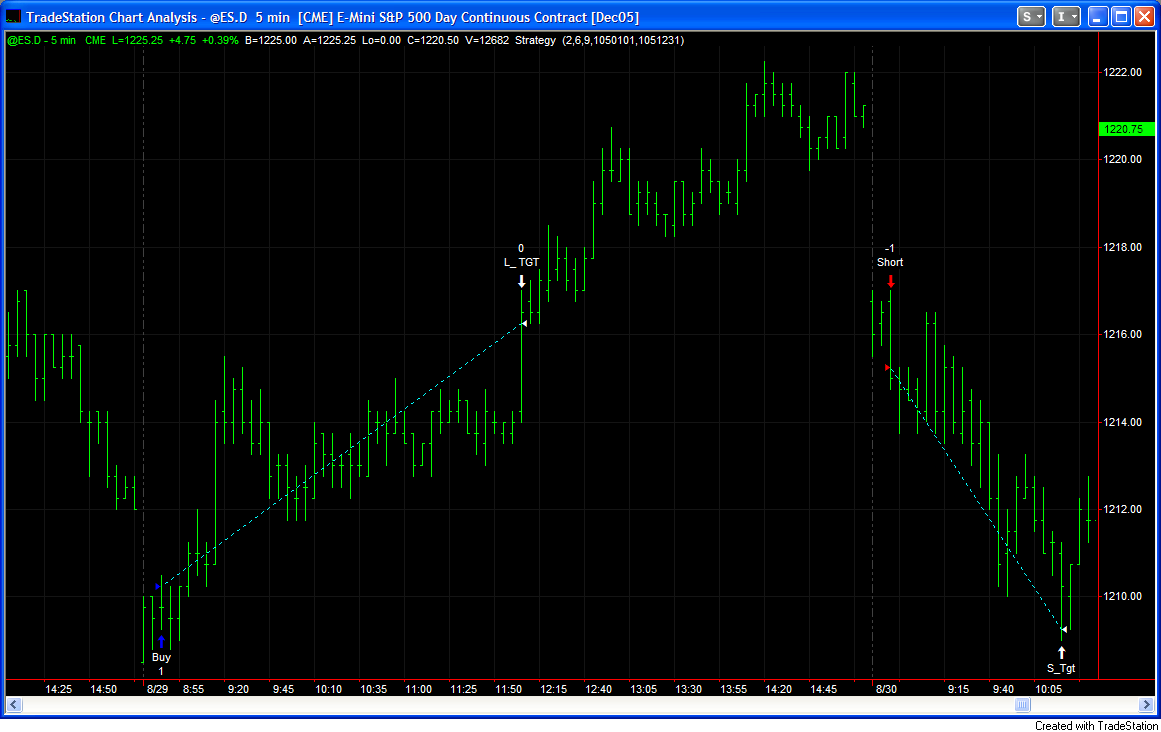

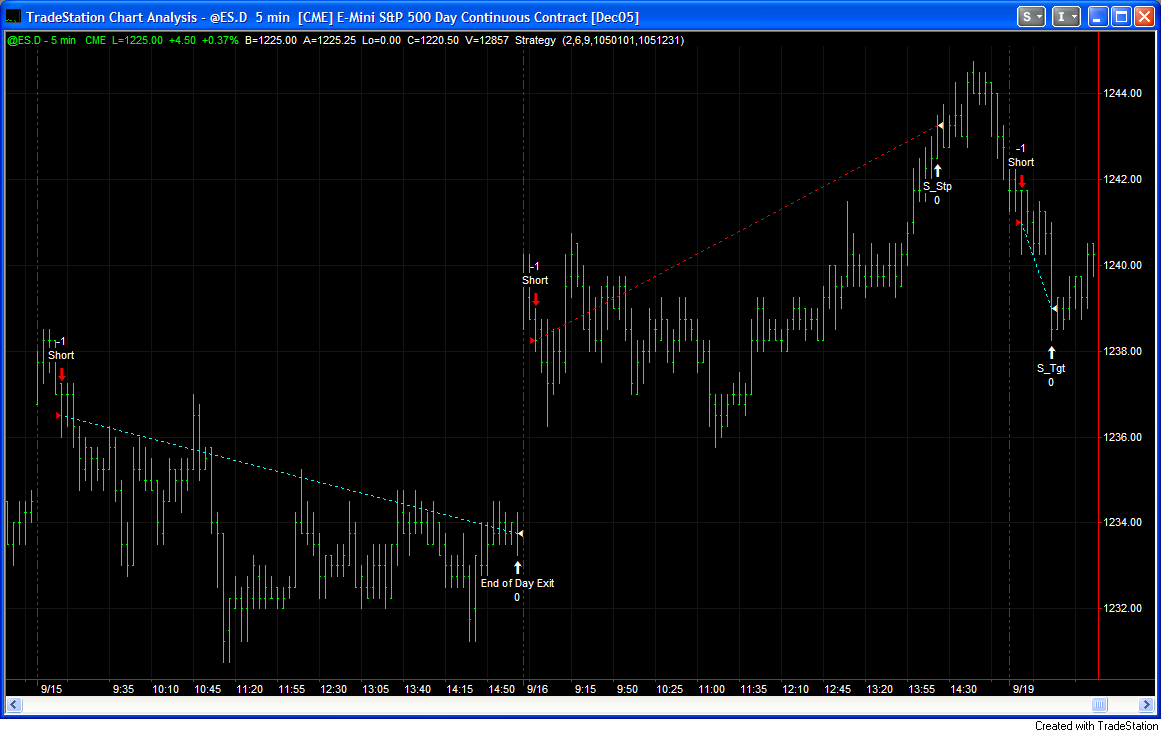

26

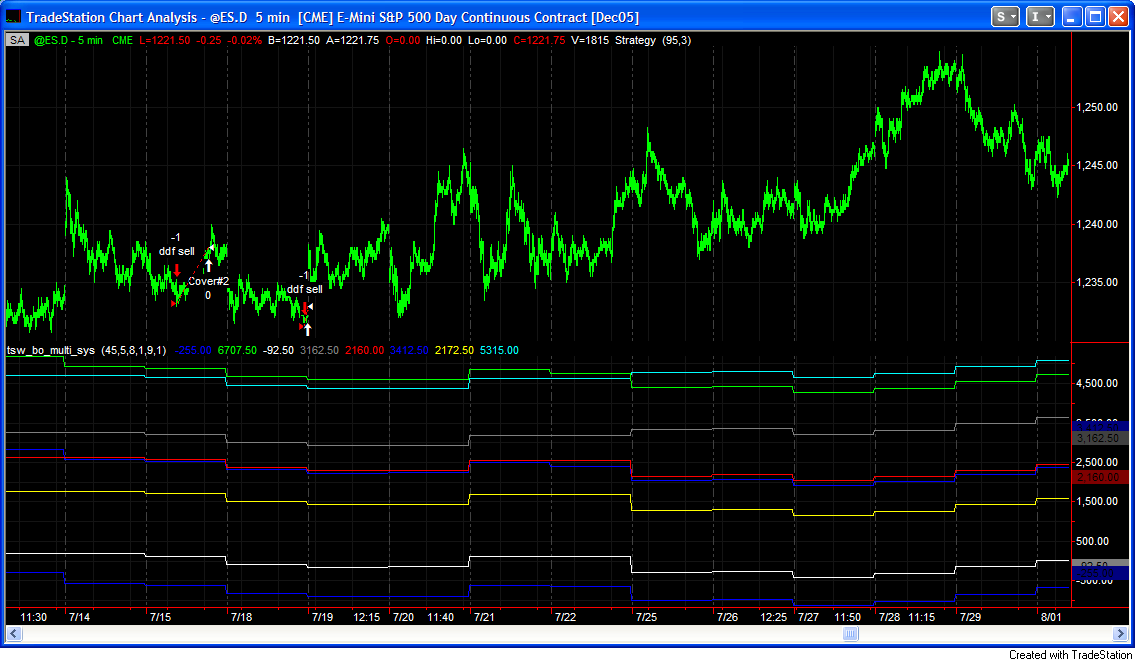

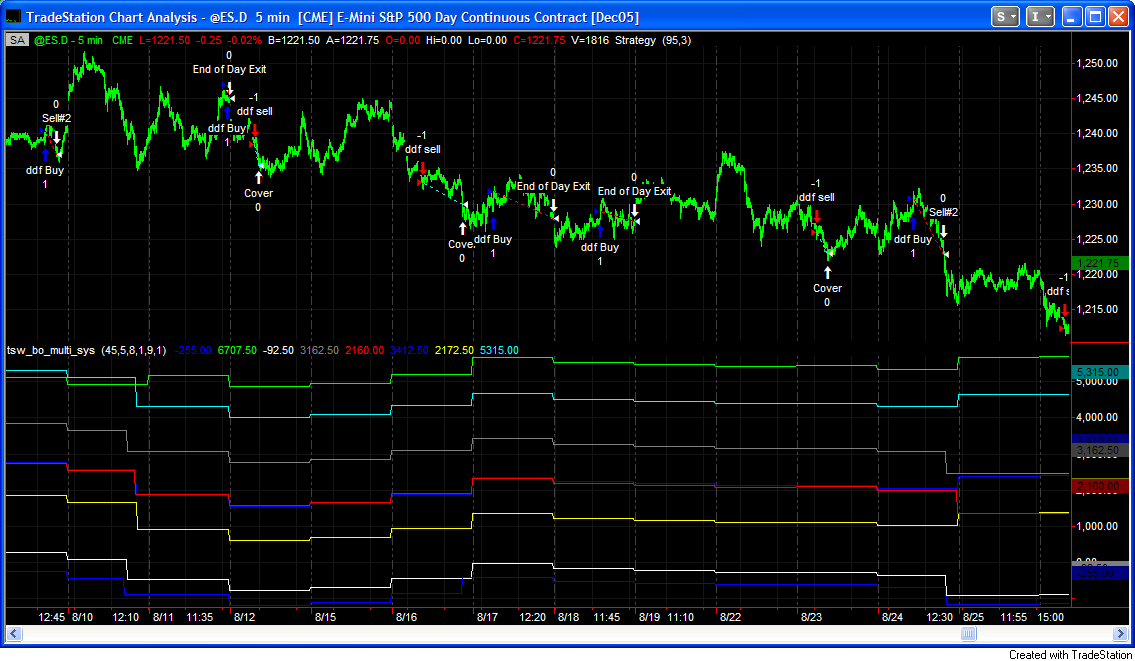

|

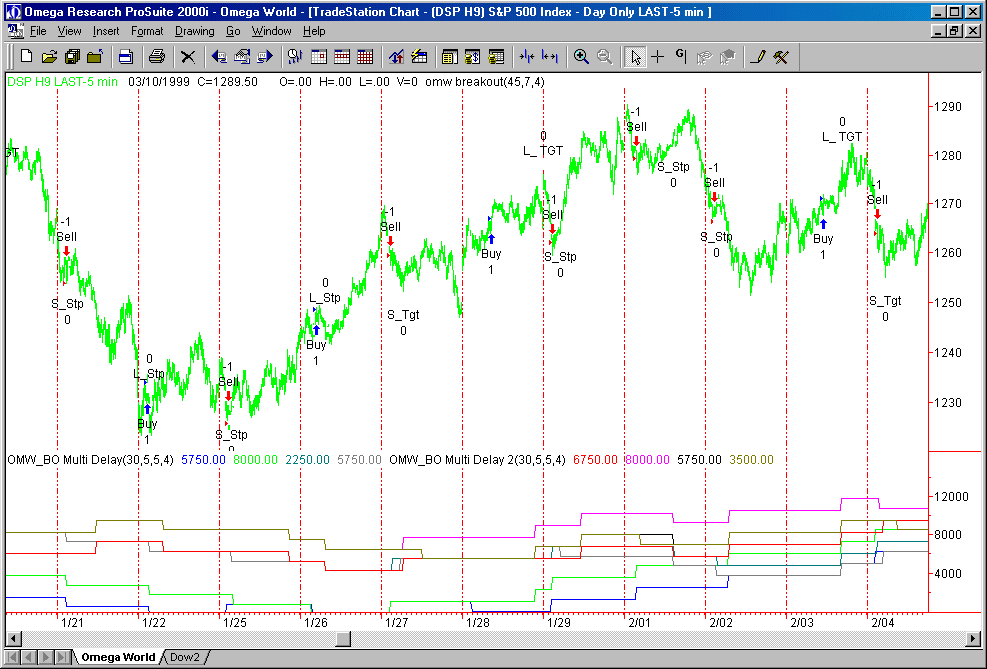

- Using a Parallel Function as an

Indicator

|

|

27

|

- Using a Parallel Function as an

Indicator

|

|

28

|

- Using a Parallel Function as an

Indicator

|

|

29

|

- Using a Parallel Function as an

Indicator

|

|

30

|

- Using a Parallel Function in an

Automated Trading System

|

|

31

|

|

|

32

|

- How does it work?

- Run multiple systems in the background, in real time.

- Set up a routine to track performances of all background systems.

- Report to the main system which settings are currently creating the

preferred trading results.

|

|

33

|

- Then simply allow the base system actually generating trading signals to

use these inputs.

- That’s it.

|

|

34

|

- System – Parallel Function Schematic

|

|

35

|

- Simple, huh?

- Well…..

- Not quite…….

|

|

36

|

- Knowing which dots to place on the wall and knowing what each dot means

is one thing.

|

|

37

|

- ??

- Connecting them to make it all

work can be quite another task.

- The programming required to

create systems of this nature is a bit more complicated.

|

|

38

|

- Step 1

- Create the parallel function.

- This is the most critical step

as the function must exactly parallel system activity.

|

|

39

|

- The parallel function must be written to deliver identical buy, sell and

exit points as the base system.

- Buy, Sell, Buy to Cover, etc. statements may not be used in functions.

|

|

40

|

- Step 2

- In the parallel function, set

up routines to test all combinations of system variables passed to the

function by the base system.

|

|

41

|

- Step 3

- Still in the parallel function,

set up sort routines to capture optimal system variable values.

|

|

42

|

- Step 4

- In the base system, set up a

routine to capture the optimal values from the parallel function and

utilize these values to generate the next trading signals.

|

|

43

|

- Day trading systems respond

best to automated re-testing each 2 – 3 weeks.

- “Swing” or shorter term overnight systems should be auto - retested

less frequently depending on the frequency of trading generated by the

system.

|

|

44

|

- As a general rule, at least 20

trades or two months time should pass between each automated system

variable reset.

|

|

45

|

- Anyone who has designed or

traded systems will readily recognize that over optimization or using an

overly restrictive testing routine often results in a significant

decrease in system performance.

|

|

46

|

- One of the advantages

realized by parallel function system testing is that the testing routine

itself can be back tested.

|

|

47

|

- In this manner one is able to

observe what the results of the system would have been had

re-optimization occurred at regular, defined intervals over specified

input values.

|

|

48

|

- Additional Considerations

- This is not a “canned”

function that can be applied to any system by simply adding a function

or separate strategy.

- It is necessary to create a

specific parallel function or functions for each system to which this

routine is to be applied.

|

|

49

|

- Additional Considerations

- This routine is not a

cure-all for a bad system. In fact, it will probably make it worse.

- Parallel function self

testing is the most effective on a sound, robust system that is showing

consistent results.

|

|

50

|

- Demo System Rules:

- 1. Buy or sell the early range breakout.

- 2. Take profits at a set target.

- 3. Use a set protective stop.

- 4. Exit end of day if no target or not stopped out.

|

|

51

|

|

|

52

|

|

|

53

|

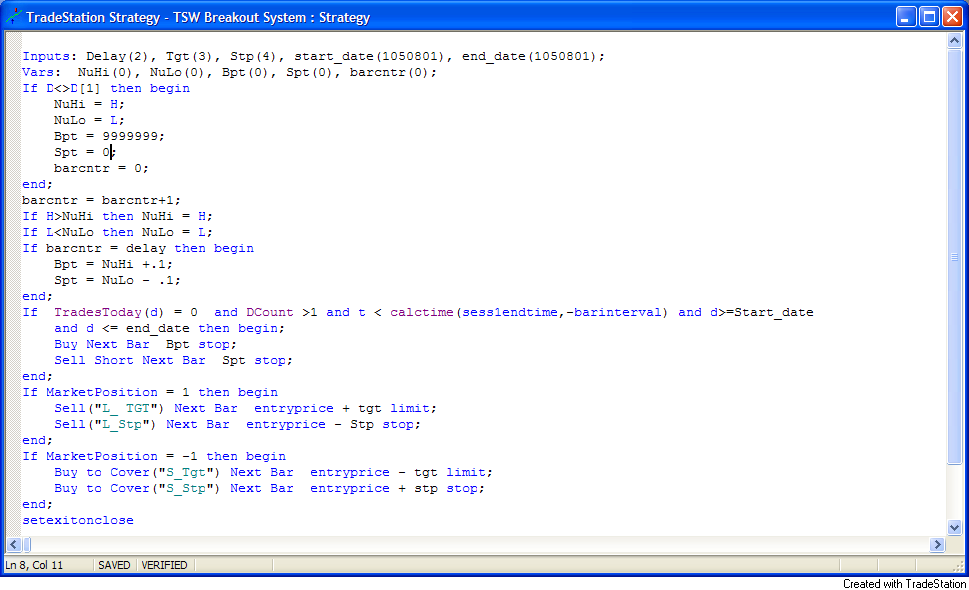

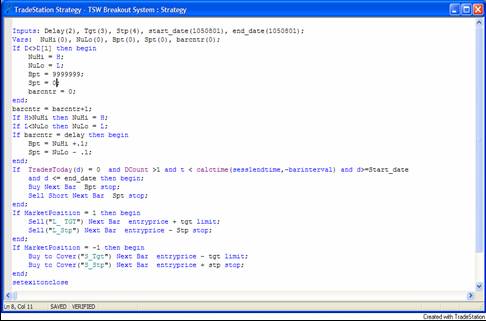

- Demo System

- Here’s the EasyLanguage Code for the demo system.

|

|

54

|

|

|

55

|

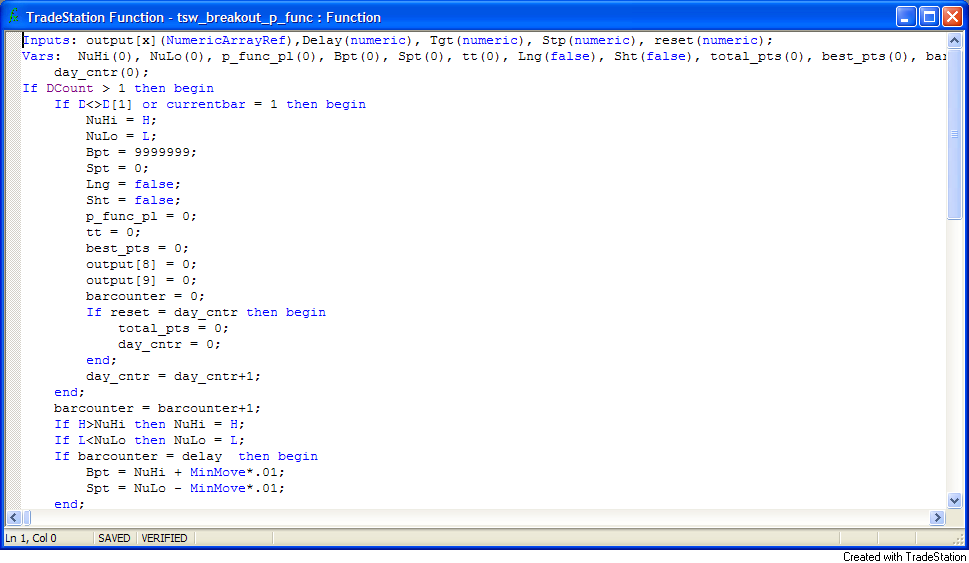

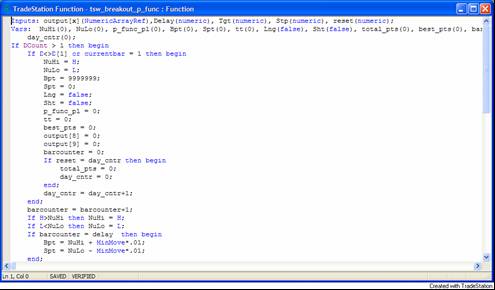

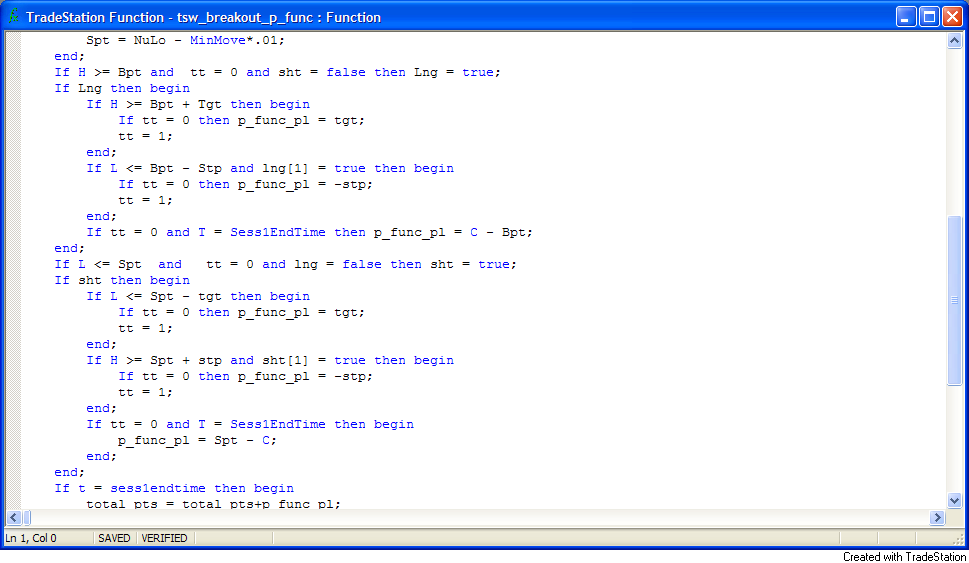

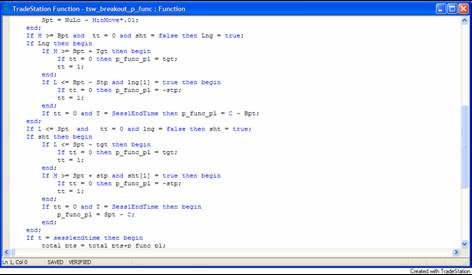

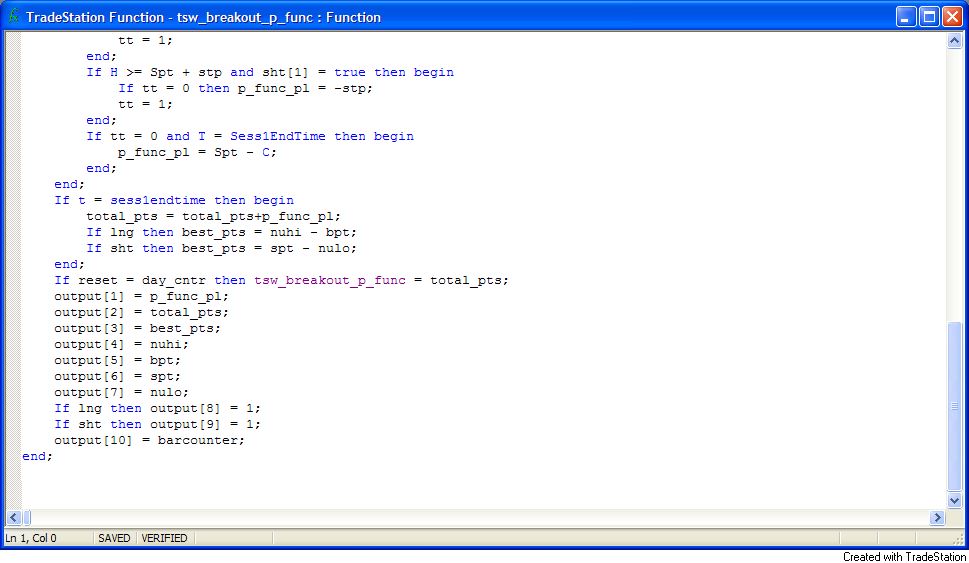

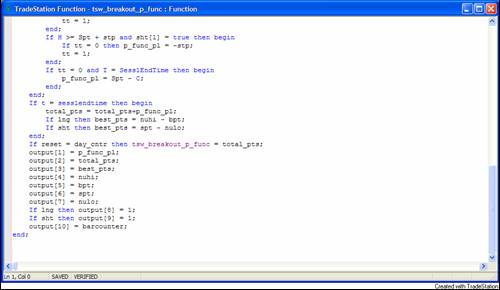

- Demo System

- Here’s the EasyLanguage Code for the parallel function that mirrors the

base system and is used to regularly check for the best system settings

|

|

56

|

|

|

57

|

|

|

58

|

|

|

59

|

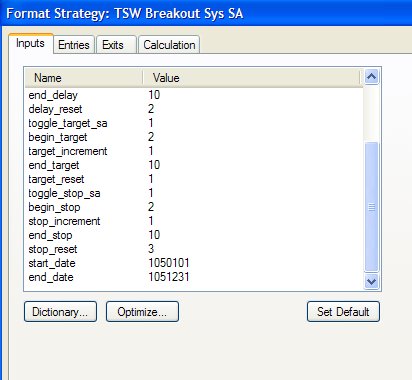

- Automated, Self Adaptive early range breakout system.

- Additional Inputs

|

|

60

|

|

|

61

|

|

|

62

|

|

|

63

|

|

|

64

|

|

|

65

|

|

|

66

|

|

|

67

|

- Now lets look at the actual system on the

e-mini S&P 500 contract

- For the purposes of this demonstration I have optimized the base system

for each parameter beginning 1-2-2005.

- We will compare the results of optimization over the last year to the

results of regular re-setting using the parallel function.

|

|

68

|

|

|

69

|

- Frequently Asked Questions:

- Is this a neural network?

- No.

- Although the parallel

function approach does use previous experiences to make real time

decisions, the process used by a neural network is significantly

different.

|

|

70

|

- Frequently Asked Questions:

- How does this approach differ

from frequent system re-optimization that can result in curve – fitting

the system to historical data?

|

|

71

|

- While frequent optimization

can certainly result in a curve fitted system, the regular, structured

and limited testing done by parallel functions will not over optimize if structured properly.

|

|

72

|

- How can you, as a trader,

make use of this technique?

- 1. This system is provided free. Trade it or better yet, use it to learn

to program your own self adaptive system.

|

|

73

|

- 2. Self adaptive indicator

packages and systems. www.clayburg.com

- Two day intensive seminars

- Oct 16 – 17 in Denver

|

|

74

|

- Managed FOREX Account

- Real Time Results Available

|

|

75

|

- Thank you for your interest.

- Dr. John F. Clayburg

- www.clayburg.com

- clayburg@pionet.net

- 712.684.5239

- 712.830.5062 cell

- Booth # 10

|

Notes

Notes{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}